SMM July 15 News:

Metal Market:

Overnight domestic base metals closed universally lower, with SHFE tin down 0.33%, SHFE copper down 0.34%, SHFE nickel down 1.08%, SHFE lead down 0.15%, SHFE aluminum down 0.15%, and SHFE zinc down 0.27%. Additionally, the most-traded alumina futures rose 1.18%, while the main continuous casting aluminum contract edged up 0.05%.

Overnight ferrous metals series showed mixed performance, with iron ore gaining 0.13% and stainless steel rising 0.08%, while rebar and HRC posted marginal declines. In the coking coal and coke segment: coking coal gained 0.05% and coke fell 0.16%.

Overnight overseas metal markets saw LME base metals closing universally lower, with LME copper down 0.18%, LME aluminum down 0.25%, LME lead down 0.82%, LME zinc down 0.22%, LME tin down 0.26%, and LME nickel down 0.88%.

Precious metals: COMEX gold fell 0.35%, COMEX silver declined 1.4% after hitting a fresh high of $39.57 per ounce during the session - the highest since September 2011. Overnight SHFE gold declined 0.05% and SHFE silver fell 0.11%.

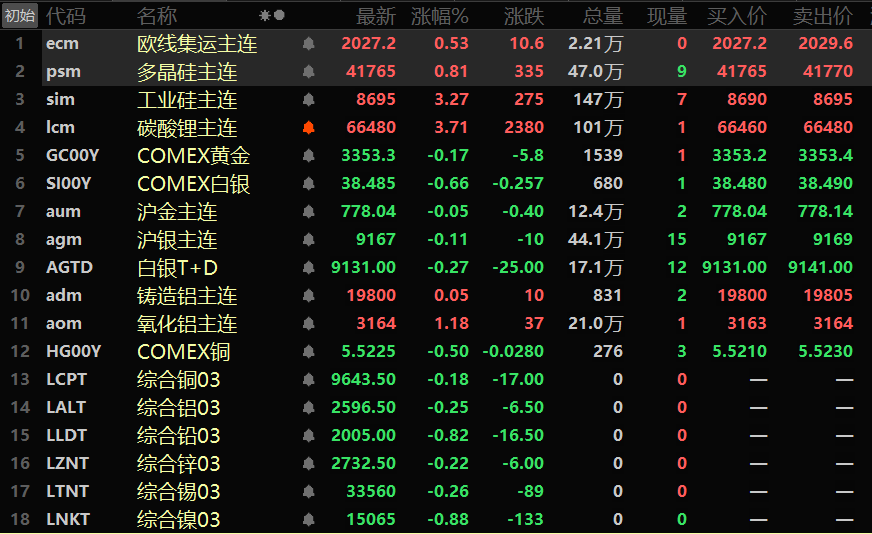

As of 7:18 on July 15, overnight closing prices

》Click to view SMM Futures Data Dashboard

Macro Front

Domestic Developments:

[PBOC Makes Key Statement on Monetary Policy, Exchange Rate, and Loan Allocation] Zou Lan, deputy governor of the People's Bank of China (PBOC), stated at the State Council Information Office press conference on July 14 that both economic theory and practical experience indicate monetary policy transmission requires time, and the effects of implemented policies will continue to manifest. Going forward, the PBOC will maintain a moderately accommodative monetary policy stance, closely monitor the transmission and actual impact of previous measures, and adjust policy implementation strength and pace based on domestic/global economic-financial conditions and financial market operations. This aims to better boost domestic demand expansion, stabilize market expectations, invigorate market entities, and support the achievement of annual economic and social development goals. Zou noted that market participants are closely watching US Fed policy shifts. Despite recent US economic growth slowdown, inflation remains above the Fed's target level, with tariff policies adding uncertainty to US inflation trajectories and affecting the Fed's interest rate cut timing. Increased volatility in the US dollar index and Treasury yields has generated spillover effects on global financial markets. By comparison, China's financial market has demonstrated strong resilience with generally stable operations, as exchange rate movements are influenced by multiple factors including economic growth, monetary policies, financial markets, geopolitics, and risk events. The current trend of the US dollar still faces uncertainties, but China's domestic fundamental economic conditions continue to improve, providing a solid foundation for the RMB exchange rate to remain basically stable amid two-way fluctuations. 》Click for details

[PBOC: H1 social financing scale increment at 22.83 trillion yuan, new loans at 12.92 trillion yuan; June M2 up 8.3% YoY]According to preliminary statistics from the People's Bank of China (PBOC), the incremental social financing scale reached 22.83 trillion yuan in the first half of 2025, an increase of 4.74 trillion yuan compared to the same period last year. Specifically, RMB loans to the real economy rose by 12.74 trillion yuan, up 279.6 billion yuan YoY; foreign currency loans to the real economy (converted to RMB) decreased by 63.8 billion yuan, with a larger decrease of 55.8 billion yuan YoY; entrusted loans declined by 51.3 billion yuan, but the decline narrowed by 40.4 billion yuan YoY; trust loans increased by 144.3 billion yuan, though the growth slowed by 165.5 billion yuan YoY; undiscounted bankers' acceptances decreased by 55.7 billion yuan, with the decline narrowing by 180.8 billion yuan YoY; net corporate bond financing reached 1.15 trillion yuan, down 256.2 billion yuan YoY; net government bond financing stood at 7.66 trillion yuan, up 432 billion yuan YoY; and domestic stock financing by non-financial enterprises totaled 170.7 billion yuan, up 49.3 billion yuan YoY. RMB loans increased by 12.92 trillion yuan in H1. Breaking down by sector: household loans rose by 1.17 trillion yuan, including a decrease of 3 billion yuan in short-term loans and an increase of 1.17 trillion yuan in medium and long-term loans; loans to enterprises/institutions increased by 11.57 trillion yuan, comprising 4.3 trillion yuan in short-term loans, 7.17 trillion yuan in medium and long-term loans, and a decrease of 46.4 billion yuan in bill financing; loans to non-bank financial institutions increased by 33.1 billion yuan. PBOC data showed that as of end-June, broad money (M2) balance reached 330.29 trillion yuan, up 8.3% YoY; narrow money (M1) balance stood at 113.95 trillion yuan, up 4.6% YoY; and currency in circulation (M0) balance reached 13.18 trillion yuan, up 12% YoY. Net cash injected into circulation in H1 totaled 363.3 billion yuan.》Click for details

[PBOC: Will conduct 1,400 billion yuan outright reverse repo operations on July 15]To maintain ample liquidity in the banking system, the People's Bank of China will conduct 1,400 billion yuan outright reverse repo operations on July 15, 2025, using fixed-quantity, rate-based tenders with multiple price awards. This includes 800 billion yuan in 3-month (91-day) operations and 600 billion yuan in 6-month (182-day) operations.

US dollar updates:

The US dollar index rose 0.25% overnight to close at 98.11. Market focus remains on trade negotiation progress and US economic data. CCTV News reported that US President Trump expressed strong dissatisfaction with Russia on the 14th local time, threatening to impose 100% tariffs on Russian imports. Trump said that if a deal cannot be reached to end the Russia-Ukraine conflict within 50 days, the US will impose "very severe, approximately 100% tariffs" on Russia. The EU and South Korea have stated that they are discussing trade agreements with US President Trump. Trump escalated the trade war on Saturday, saying that he will impose a 30% tariff on most goods imported from the EU and Mexico starting next month, after issuing similar warnings to other countries, including Japan and South Korea.

"This is something that has happened before, and the impact has faded away," said Joseph Trevisani, a senior analyst at FX Street. Meanwhile, "negative forecasts have not materialized, so I don't think tariffs will have much impact on the market," he added.

The market is currently awaiting Tuesday's US Consumer Price Index (CPI) data and Wednesday's Producer Price Index (PPI) report for clues on the potential policy path of the US Fed. Economists surveyed expect the overall annual inflation rate to rise from 2.4% last month to 2.7%. The core inflation rate is expected to increase from 2.8% to 3.0%. US federal funds rate futures traders expect a 50-basis-point interest rate cut by the end of the year, with the first cut expected in September. (Wenhua Comprehensive)

Data:

Today, data such as China's year-to-date urban fixed asset investment annual rate for June, China's year-to-date industrial added value annual rate for enterprises above designated size for June, China's year-to-date total retail sales of consumer goods annual rate for June, China's Q2 GDP annual rate for the quarter, China's Q2 GDP year-to-date annual rate, the Eurozone's July ZEW Economic Sentiment Index, Germany's July ZEW Economic Sentiment Index, the Eurozone's June total reserve assets, the US's June CPI annual rate (unadjusted), the US's June core CPI annual rate (unadjusted), the US's July New York Fed Manufacturing Index, Canada's June unadjusted CPI annual rate, Canada's June core CPI - common annual rate, Canada's May manufacturing sales monthly rate, and Canada's May manufacturing new orders monthly rate will be released.

In addition, attention should be paid to the monthly report on residential sales prices in 70 large and medium-sized cities released by the National Bureau of Statistics (NBS); the State Council Information Office's press conference on the national economic operation; a speech by 2025 FOMC voting member and Boston Fed President Susan Collins; a welcome address by Fed Governor Michelle Bowman at a conference hosted by the Fed; and speeches by Bank of England Governor Andrew Bailey and Chancellor of the Exchequer Rachel Reeves at a dinner at the Mansion House in London.

Crude oil:

Both WTI and Brent crude oil futures fell overnight, with WTI down 2.37% and Brent down 1.73%. The market is weighing the new threat of US President Trump's sanctions on Russian oil, which could affect global oil supplies, while remaining concerned about Trump's tariff policies.

Industry insiders said that Russia's seaborne exports of petroleum products fell by 3.4% in June from May to 8.98 million mt. Meanwhile, EU envoys are on the verge of reaching an agreement on the 18th round of sanctions against Russia, which includes lowering the price cap on oil. According to CCTV News, Slovak Prime Minister Fico stated on social media on July 14 local time that the European Commission had proposed a written guarantee to Slovakia as a condition for the country's support of the 18th round of sanctions against Russia. It is understood that the proposal includes providing safeguards to Slovakia after the EU gradually stops importing natural gas from Russia, so that it can purchase natural gas at reasonable prices.

A preliminary survey showed that US crude oil and gasoline inventories were estimated to have declined last week, while distillate inventories may have increased. Before the weekly inventory data was released, the average forecast of five analysts surveyed was that US crude oil inventories were expected to decline by about 1.6 million barrels in the week ending July 11. Analysts surveyed estimated that distillate inventories, including diesel and heating oil, increased by 700,000 barrels, while gasoline inventories declined by about 700,000 barrels in the week ending July 11. The American Petroleum Institute (API) will release its weekly inventory report at 4:30 Beijing time on Wednesday, and the US Energy Information Administration (EIA) will release its weekly inventory report at 22:30 Beijing time on Wednesday. (Wenhua Comprehensive)